Learn all the hacks to upgrade and optimize your life, money and travel – all while spending less and saving more.

💰 Spending & Cash Flow: Apps, Tools, Tips and Tricks

Hello Reader,

It’s no secret I've been on this journey to optimize my finances, seeking ways to save money while still enjoying the things that matter most.

Today, we're diving into one aspect of financial optimization: spending and cash flow.

It's not about frugality; it's about making informed choices, understanding where your money flows, and ultimately having more control over your financial destiny.

By the end of this newsletter, you'll learn:

- The importance of budgets and tracking

- The best software tools to simplify the process

- Proven tactics to set up your financial system

- Tips and tricks to deal with some (likely) challenges

- The two questions you need to ask yourself for success

This is a timely post because this week Intuit announced their budgeting tool Mint will be no more – it’s big news impacting over 3 million users. If you’re one of them, I have some advice for you below :)

|

Today’s newsletter is brought to you by… Henson Shaving

Henson is an aerospace parts manufacturer that brings its precision engineering expertise to a razor, which enables a blade extension of precisely 0.0013”, resulting in an incredibly smooth and pleasant shave.

I spent a week using my Henson on one half of my face and my overpriced cartridge razor on the other and I can confidently say it’s a superior shave. And it’s such a better deal, because once you own a Henson razor, it only costs ~$3-5 per year to replace the standard dual-edged blades.

To get a razor that’ll last a lifetime and 100 free blades, go to allthehacks.com/henson and use the code ALLTHEHACKS (don’t forget to put the blades in your cart).

🤑 Why Tracking Your Spend Matters?

Most people I know monitor and track their account balances and net worth, but I find only a handful of them actually know how much they spend each month.

Tracking your spending allows you to be more deliberate in your decisions and better understand your future financial picture. And the simple act of tracking can enable you to make changes and save more money.

Budgeting vs. Spending Tracking

While “budgeting and spending tracking” may seem synonymous, the two have an important difference.

- Budgeting involves establishing specific spending targets and ensuring your spending aligns with those targets.

- Spending tracking is a more passive/reactive approach where you focus more on tracking what you’re doing and making adjustments later.

Amy and I focus much more on spending tracking, but we do make a budget, just not for the typical reason. For us, the budgets act as a monthly or annual target for spending that we can compare to reality each month/year. It helps us gauge whether we are spending more than we were planning.

💵 Spending Tracking Tools

When tracking your spending, there are so many tools at your disposal (plus new ones keep popping up regularly). I first started with Mint, but categorizing transactions was so frustrating. Then I tried a manual spreadsheet, but that became too time-consuming, so I restarted the Mint account again with fresh eyes, but it wasn’t “easy” enough to keep it up.

However, as All the Hacks transformed into a permanent endeavor and Amy and I left our jobs, we decided it was time to try again. So we invested A LOT of time finding the right tool that required the least effort to get good data, and I’m so glad we did.

How These Tools Work

While many apps for budgeting and spending tracking allow you to enter everything manually, I think that’s way too much work and would be near-impossible to maintain. Instead, I prefer an automated tool that connects with my bank accounts and credit cards to pull in all my transactions.

Most of these tools rely on data aggregators like Plaid, Yodlee, or MX to collect your financial data. Typically, you share the login credentials for your financial institution to the aggregator, who regularly pulls your transaction data and shares it with the app you’re using. Recently, some institutions have adopted Open Banking, which allows you to authorize read-only access to your data without needing to share your login credentials, but right now, there are only a few of the major institutions that support this.

Personally, I trust using these aggregators to connect my accounts with all the finance apps I use. However, if I’m ever using an app that asks for my credentials directly instead of through a popup operated by an aggregator like Plaid, I would stop using the app immediately.

I’m telling you this because security is paramount. If you’re ever prompted to enter your credentials to link accounts, make sure it’s a trusted aggregator or the financial institution itself.

Tools Experimentation

So, as I said, I was committed to finding the best tool for myself (and to help you all), so I decided to open an account with each of the following tools earlier this year and even synced all my financial transactions from 2022 from all my accounts.

- Copilot

- Monarch Money

- Mint

- Rocket Money

- TIllerHQ

- YNAB (You Need A Budget)

- SimpliFi (Quicken product)

The tl;dr of that process was that I found Copilot to be the clear winner and have been using it almost every day for the past six months. Naturally, once I decided it was the best product for me, I decided to reach out to them to see if they would partner with All the Hacks, which they did, so you all can get 2 months free with the code HACKS2. However, just to be clear, they are not paying me to produce this newsletter, and they had no input into the content or the highlights from all my testing:

- Copilot ($95/year, but 2 months free with HACKS2) has speed, user-friendly design, versatile functionality, and automatic categorization (using a personal AI/LLM model from your date). Even better, they built a few features to help manage some common issues, like tracking Amazon purchases, Venmo transactions, and variable monthly budgets. All this made it the best option for us; however, it is only available on iOS and Mac devices.

- Monarch Money ($99/year) was another option that worked on more platforms (Android and web), but once I had a lot of transactions imported, the web interface felt slow. I also had a strong preference for the Copilot UI/UX. That said, it might be a good option if you’re an Android user or want to manage budgets and track spending from a Windows computer.

- Mint (free) was a popular choice for years until it announced that it would be shutting down and transitioning its functionality to its sister product, Credit Karma. The good news is that Copilot and Monarch will soon both have tools to import any of your previous Mint transactions.

- Rocket Money (free) was already an app I had used to cancel subscriptions and automate bill negotiations, but it wasn’t until this process that I decided to really put its tracking functionality to the test. I was pretty impressed with the product, but it lacked some of the customization features I was looking for and was impossibly slow to manage a large amount of historical transactions. That said, it was the best free tool I found.

- TillerHQ ($79/year) is designed for the spreadsheet lover and basically sits as a technology interface to the aggregators and pulls all your transactions directly into Google Sheets or Excel. It has a steep learning curve, but if you want everything in a spreadsheet, you should check it out.

- SimpliFi ($48/yr) earned recognition as Wirecutter's top pick, but many of the apps above weren’t even tested, so I’m not sure how much to read into it. Personally, I found it way too complicated to use. For example, transactions don’t link to any budget or tracking until you manually create a separate spending plan (requiring you to then add them again one by one). I even watched every SimpleFi video I could find on YouTube, but I couldn’t find anyone that made it look easy to use or worth spending more time on.

- YNAB ($99/year) uses a zero-balance budgeting approach, which isn’t for everyone. It means that instead of just tracking what’s happening, you need to assign every dollar of income to a specific purpose (e.g., expense, saving, debt payment). It’s great for those who want to budget like that, but it’s not for me. To learn more about YNAB's philosophy, check out 🎧Ep 16 with their CEO.

✅ Setting Categories

Regardless of the tool you use, categorizing your spending is vital to managing your finances effectively, and the setup for most tools is quite similar. The primary goal is to ensure that every expense you have is tied to a particular category so that you can analyze your spending later.

Most tools provide a default set of categories you tweak as much as you’d like. The level of detail you require is a personal decision. For instance, you might not need to differentiate between various dining expenses, such as coffee shops, bars, restaurants, or fast food. You may simply want to know the total spent on “dining.”

It's essential to remember that making things too complicated might make the whole process unsustainable. So, I’d suggest erring on the side of simplicity when starting and deciding later if you require more categories.

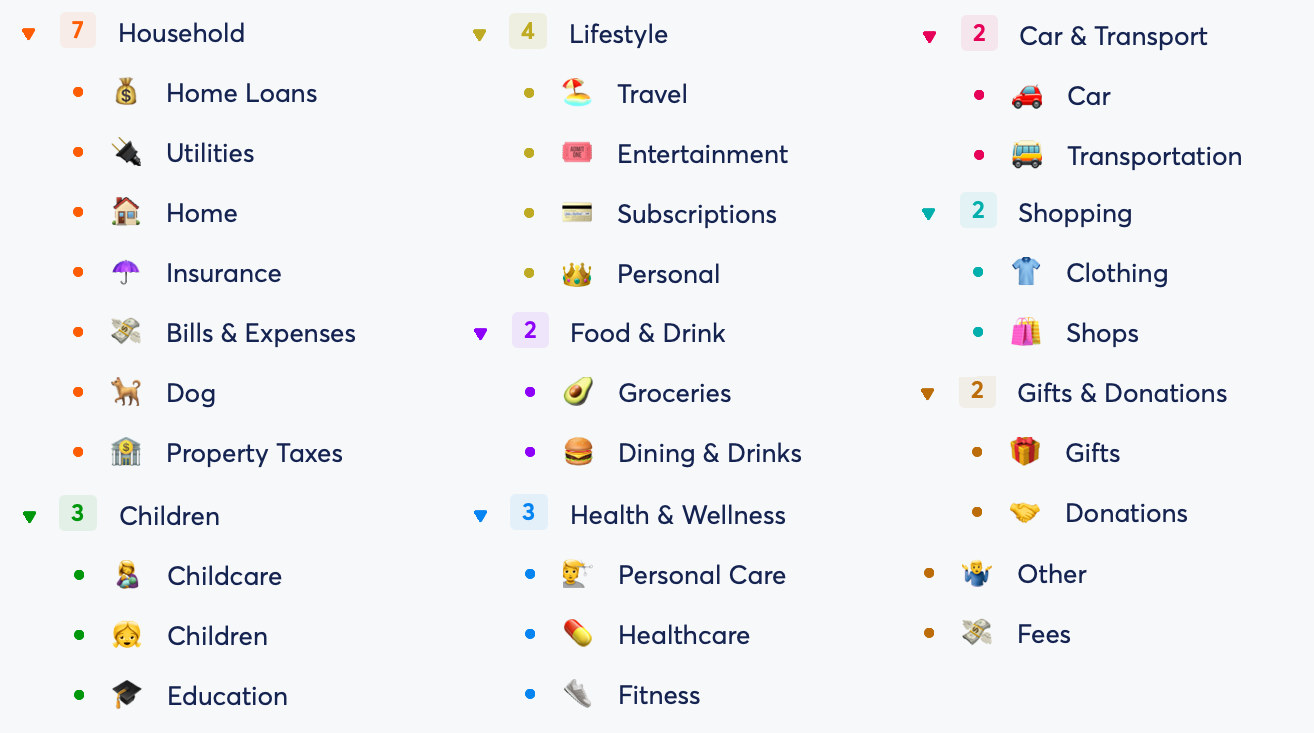

Our Categories (and subcategories)

In case it’s helpful, here’s the set of categories we ended up with:

|

Then, for each category, I have a specific budget set. Most of them default to a monthly basis – but some give you the flexibility to go in and set different budgets for each month. This matters for expenses like property taxes that I have to pay semi-annually.

Note on fees: This is almost entirely credit card annual fees, but any time I get a credit for purchases (e.g., Chase Sapphire $300 travel credit or Amex Platinum Saks Credit), I put the credits in “Fees” as well to offset the annual fees.

🧮 Tips & Tricks for Categorizing & Tracking

After all the setup is complete, the monthly task is to categorize transactions. Most apps do a decent job of auto-categorizing to their default categories, but you can usually set up your own rules that will auto-categorize specific merchants/amounts to a specific category and save you time in the future.

Once you have the process down, this only takes a few minutes to complete each week.

However, some other issues might come up along the way, so here are a few I went through and how you might deal with them.

Multi-Category Retailers

Some retailers (e.g., Target and Amazon) sell everything from clothing to groceries to electronics and may not fit perfectly in one category.

You can take the simple approach where you lump an entire retailer into its category or spend more time diving into the itemized transactions and categorizing them correctly.

For Target, we’ve opted for a straightforward approach. We use the category "Shops" and place all expenses related to this store there. We took this approach because much of what we spend at Target is relatively similar, and to be honest, "Shops" could probably just be “Target.”

That is different, however, when it comes to Amazon. We buy a wide range of items that we’d like to keep separate. Fortunately, there are two good options for making it easy to categorize Amazon purchases:

- Go to the transactions page, where everything is sorted by credit card charges instead of orders: Go to “Account & Lists” => “Account” => “Your Payments” => “Transactions”

- If you use Copilot, they have an Amazon integration where you can sync your Amazon account with the Copilot app, and they’ll show the individual items within the transaction, making it really easy to categorize.

|

Handling Refunds

Refunds sometimes pose a challenge when it comes to accurate expense tracking when the timing is spread across multiple months (e.g., purchasing a holiday gift in December but returning it in January). This means you’ll still have that expense in one month and a negative transaction the next month. I try to manually backdate the refund charge to be in the same month as the original transaction, ensuring that the expenses cancel each other out in the same month.

ATM and Spending Cash

You all know I love points, so I rarely spend cash, but sometimes when traveling abroad, it’s necessary. The most common advice would be to categorize the ATM withdrawal as a “transfer” and then manually enter every cash transaction with the right category. That seems like too much work for me, so if I’m withdrawing cash on a trip and most of it was used for food, I’ll just categorize it all as “Dining and Drinks” and not worry about some of it being spent in another category. While this isn’t perfect, it's far more convenient than manually logging each cash transaction.

Venmo

Venmo and other P2P payment app transactions can also be a source of confusion because they often maintain their own balance, so if you receive $50, send $30, receive $20, and then cash out, you’ll just see a $40 deposit. I’ve had limited success with using aggregators to sync with Venmo, so here are two options:

- Be diligent about always cashing out your balance so it’s always at $0, and every payment (sent or received) ends up hitting your checking account.

- If you use Copilot, they’ll create an email address; you can use email filters to auto-forward your Venmo transaction receipts so they can add them all as transactions to your account.

Rollover Budgets

One challenge with most tools I’ve used is that they require monthly budgets. That works well for many things, but there are some categories, like Travel, where the bulk of the spending happens in a few months of the year that aren’t always the same. The simplest way I’ve found to solve this is to enable rollover budgets (assuming the tool you pick allows it), which just roll over any leftover money in the budget to the next month.

Some tools even let you selectively choose which categories utilize rollover budgets and which do not, providing you with the flexibility to manage variability in your expenses each month effectively.

Non-Monthly Recurring Payments

One category of transaction that always tripped me up was larger semi-annual or annual expenses, like Car Insurance or Property Tax. While you could use rollover budgets for this, I didn’t think it was a perfect solution. However, the advice I frequently found online was to take a payment like semi-annual insurance and split the transaction into six transactions (then change the dates to spread them out over six months). This seemed like a lot of administrative work, so here are two easier alternatives:

- Some insurance companies (thanks, USAA!) let you pay monthly for no additional fee, so you can do that and not worry about it.

- Some tracking tools will let you change your budgets every month. So I have my Property Tax budget in Copilot set up to be $0/month for 10 months of the year and then much higher the two months I have to make our semi-annual payments.

🏆 Why Spend The Time Tracking? (Benefits!)

The real value in all of this is in the insights that come from doing the tracking.

You can understand your spending patterns comprehensively – and examine your expenses on both a category and subcategory level, revealing where your money goes each month. This information empowers you to assess whether your current spending aligns with your financial goals and priorities.

For Amy and me, it enables us to think about two very important questions:

- If we were going to spend more money, where would we put it (i.e., is there a category where we feel like we're too restrained)?

- If we were to cut from our current spending, where would we cut?

It allows us to think about where we would spend more or less – and make the adjustments to align with the lifestyle we want to embrace.

While budgeting and expense tracking may require time and effort, their many advantages can significantly enhance your financial well-being and decision-making.

Finding a balance that works for you and your unique financial goals is important.

🎙️ More on Optimizing Your Finances? Check this

If you enjoyed this post, I suggest diving deeper down the rabbit hole:

- Listen to this podcast – (🎧 Ep. 9) How to Live Your Rich Life

- Read this newsletter post – 📰 5 Ways to Optimize Your Money

And if you want even more ways to save money in each category, listen to (🎧Ep.133) Mastering Cash Flow: Tracking Spending to Boost Savings and 10+ Hacks to Spend Less

💭 Parting Thoughts

I hope today’s newsletter gives you the framework for a simpler, more effective tracking strategy. A little investment in time will go a long way and enable you to become a better saver and spender.

If you have any unique tips or hacks for managing spend, please feel free to share them with us by replying to this email or sending me a note at podcast@allthehacks.com!

Special thanks to our partners Henson Shaving and Copilot

All the Hacks

by Chris Hutchins

Learn all the hacks to upgrade and optimize your life, money and travel – all while spending less and saving more.

Hi Reader, Turns out the majority of our communication is spontaneous. It is rarely planned except for our formal presentations, pitches, or meetings. In the spur-of-the-moment we often feel anxiety because the urgency, desire for precision, and need to adapt to the situation converge simultaneously. Good news! Successful spontaneous speaking, whether it's answering questions, providing feedback, or engaging in small talk, is a skill everyone can refine. I recently spoke with Stanford...

Hello Reader, We've all made our fair share of poor decisions (I know I have), so I want to talk about improving our decision-making. I had the chance to interview Annie Duke (🎧Ep 81) at the end of 2022 about changing how you approach your choices. Annie is the author of bestsellers Thinking in Bets: Making Smarter Decisions When You Don't Have All the Facts and Quit: The Power of Knowing When to Walk Away. Today, we’ll get actionable and uncover 10 ways to improve decisions and understand...

Hi Reader, Last year's gift guide was a huge hit, so I wanted to put together a 2023 Gift Guide with over 50 of my favorite products, gifts, past purchases and more. Hopefully some of them might make good ideas for gifts this holiday season. I broke the list into the following sections: 🏡 Home & Food 🧑🔧 Tech & Gear 👕 Clothes & Bags 🏃 Health & Fitness 👨👩👧👦 Family & Kids 📖 Books & Learning 💰 Saving Money When You Shop Unfortunately the list was too long and/or had too many links for email, so...